Apple: A Purchase Into Q3 Earnings, Refresh Cycle Helps The New Development Story (AAPL) – Cyber Tech

kyotokushige/DigitalVision by way of Getty Pictures

Apple (NASDAQ:AAPL) typically will get chastised for its lofty valuation. In any case, shares commerce at a mid-20s earnings a number of even when utilizing 2026 working EPS estimates. I see tailwinds, although. Contemplate that the launch of Apple Intelligence (its personal “AI”) and the fact that a pc refresh cycle is probably going on the best way, now that we’re 4 years faraway from the at-home electronics shopping for binge throughout COVID, doubtless means an earnings development restoration story is on the best way.

Forward of the $3.3 trillion market cap firm’s earnings report Thursday night time, I’ve a purchase ranking on the inventory with a worth goal of $245. I see basic upside, whereas its technical scenario seems first rate after a key long-term breakout earlier this 12 months.

Apple Highlights a Large Week of Earnings

Wall Road Horizon

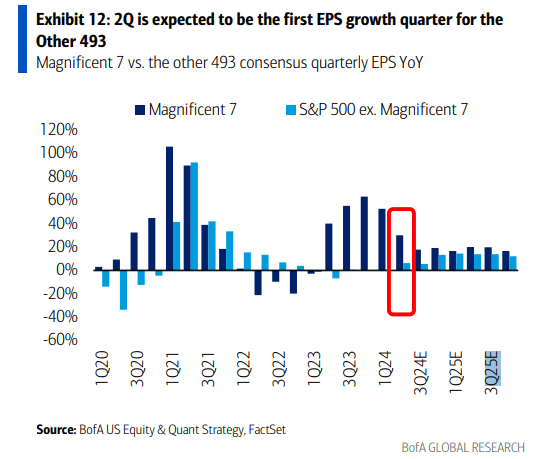

Whereas S&P 493 EPS Development Could Flip Comparatively Excessive, AAPL Earnings Ought to Additionally Improve Subsequent 12 months

BofA International Analysis

As a refresher, Apple reported a strong Q2 report again in Could. Non-GAAP EPS of $1.53 beat the consensus estimate of $1.50 whereas income of $90.8 billion, down 4.3% from year-ago ranges, was a small $190 million beat. It was the fifth consecutive bottom-line beat, regardless of the flat EPS pattern over the previous two years. Shares jumped 6% the next session – the perfect response to earnings going again to October 2022. Since then, there was a gentle weight-reduction plan of sellside EPS upgrades, offering a basic increase to what has turned out to be a technically robust chart.

CEO Tim Prepare dinner and the remainder of the administration crew introduced a report $110 billion share repurchase authorization and a 4% dividend hike in early Could, each shareholder-friendly strikes have been acquired effectively by the market. However the firm’s working margins have been combined throughout geographic areas – China was a weak spot in that respect as a result of aggressive pricing and rising competitors, particularly from Huawei.

Whereas there have been some regulatory challenges, together with a pair of EU investigations and up to date rumors of a home clampdown from the US Division of Justice, these ought to show to be fairly immaterial to the long-term profitability trajectory.

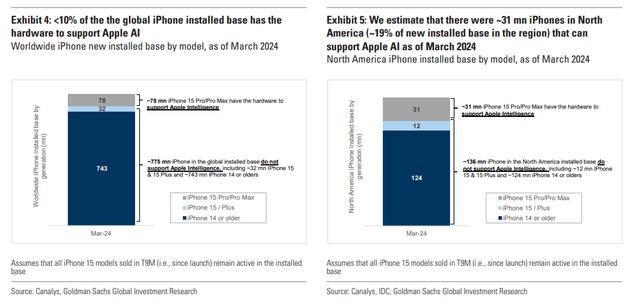

What’s extra pivotal right now is the AI story and the potential for a major iPhone and Mac refresh cycle that would drive income and earnings within the quarters to come back, although the upcoming quarterly report will doubtless present a year-over-year drop in iPhone gross sales.

Analysts at Goldman Sachs count on Mac income to surge 13% from the identical interval a 12 months in the past, with near flat numbers within the wearable area. Companies income is seen rising at a mid-teens fee amid strong app retailer spending by customers.

Apple’s Large Set up Base Means Main Refresh-Cycle Potential

Goldman Sachs

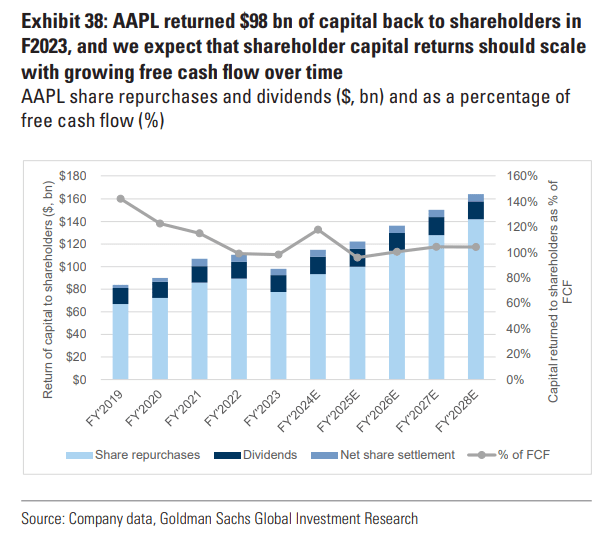

Greater image, I assert that traders typically get misplaced in what’s a really constructive monetary engineering story. Apple returned almost $100 billion to shareholders final 12 months alone. That quantity is forecast to develop in FY 2024 as the corporate produces market-leading free money move.

So, at the same time as earnings have ebbed in recent times, EPS can nonetheless develop considerably due to the buyback story. Then, as I consider will happen, a bullish working backdrop can resume within the years to come back given Apple’s strong set up base and recurring income.

Apple: Continues to Reward Shareholders

Goldman Sachs

The Choices Angle

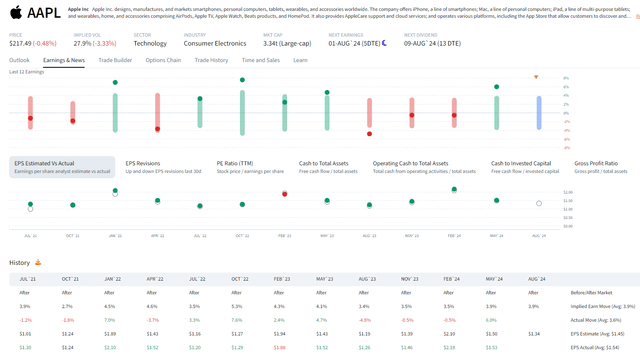

As for the quarter to be reported, knowledge from Choices Analysis & Expertise Companies (ORATS) present a 3.9% earnings-related inventory worth swing priced into the straddle expiring after the report.

That’s according to the final dozen EPS experiences, whereas the consensus EPS estimate is $1.33 on an working foundation which might be a 6% improve from Q3 2023. The corporate has averaged a seven-cent beat within the final 5 quarters, so the whisper quantity is probably going about $1.40.

A 3.8% Straddle Into Earnings

ORATS

Funding Score Dangers

Key dangers to my purchase ranking embrace weaker client spending and ensuing softer demand for Apple’s extra discretionary services and products. Competitors continues to develop in each the {hardware} and companies areas, too, which may threaten margins if it persists greater than the market expects.

Regulatory dangers are current with a big agency like Apple, whereas clear provide chains are important for the multinational company. It’s additionally key that the administration crew continues to execute effectively on each inside tasks and with M&A.

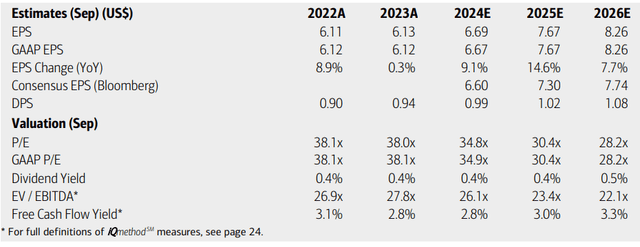

Ahead Numbers

On the earnings outlook, analysts at Financial institution of America International Analysis see working EPS rising 9% this 12 months after a flat 2023. Per-share earnings are then anticipated to speed up to a virtually 15% clip within the out 12 months, with still-solid 9% earnings development by FY 2026. The present Searching for Alpha consensus numbers present a comparable EPS trajectory however with a extra balanced earnings development fee via 2026. Gross sales are forecast to extend by 7.4% subsequent 12 months, after only a 1.1% rise in FY 2024.

Dividends, in the meantime, ought to develop at a gentle tempo over the quarters forward, whereas the agency’s free money move yield might eclipse 3% ought to the inventory worth maintain its present stage.

Apple: Earnings, Valuation, Dividend Yield, and Free Money Circulate Forecasts

BofA International Analysis

If we assume ahead 12-month EPS of $7.50, which I assert is achievable given the robust companies and potential {hardware} refreshes, and apply a low-30s earnings a number of, then shares ought to commerce close to $245. That P/E is above the mid-point of its historic vary, however I see that as warranted given the multi-year refresh cycle about to start, the agency’s fortress stability sheet, and a extra numerous mixture of product and repair choices.

Goldman writes about the potential for $9 to $10 of NTM non-GAAP EPS, however which may be out of attain given the latest trajectory, and we’ll know extra after this Thursday night time. Additionally contemplate that the consensus is for $8.22 of FY 2026 EPS – a 30x a number of would put the inventory close to $260 by September subsequent 12 months.

Apple: Not A Low-cost Inventory, However Attractively Priced On A Ahead Foundation

Searching for Alpha

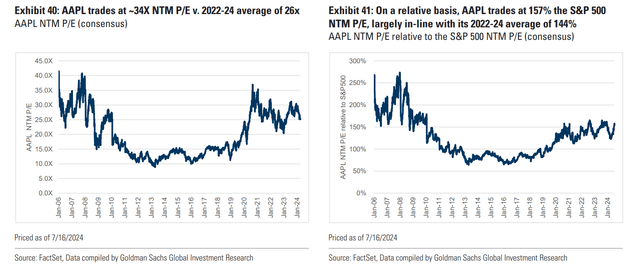

AAPL: P/E A number of Historical past, Absolute & Relative Appears

Goldman Sachs

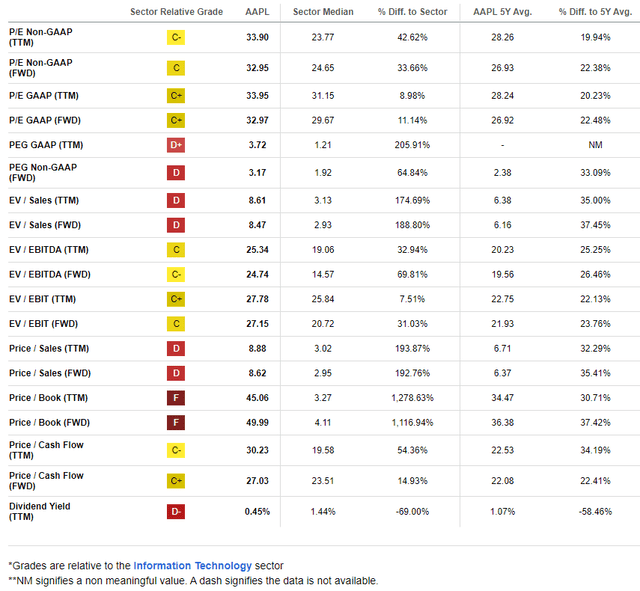

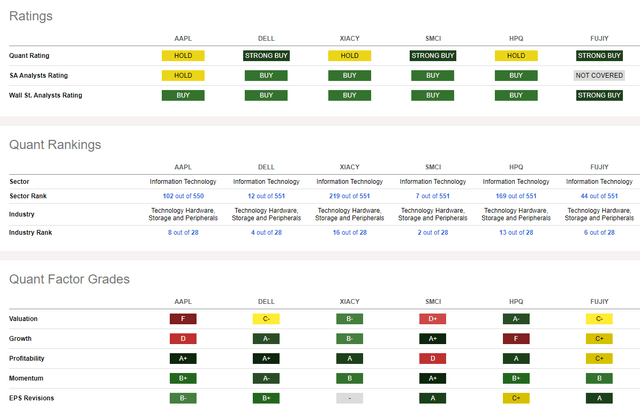

In comparison with its friends, AAPL sports activities a weak valuation, however I contend that its commanding trade presence, excessive and sustainable margins, and consumer-staple-like penetration in customers’ lives is exclusive. What’s extra, the P/E a number of premium shouldn’t be all that rather more vital than the common of the remainder of the Magnificent Seven.

The expansion trajectory has been lackluster currently, however that’s set to inflect constructive, which ought to present bullish headline potential. With stout profitability tendencies and powerful share-price momentum, I see AAPL as a deserving core holding for traders. Lastly, EPS revisions have been to the great facet up to now 90 days, a pattern I consider will persist via the Q3 report.

Competitor Evaluation

Searching for Alpha

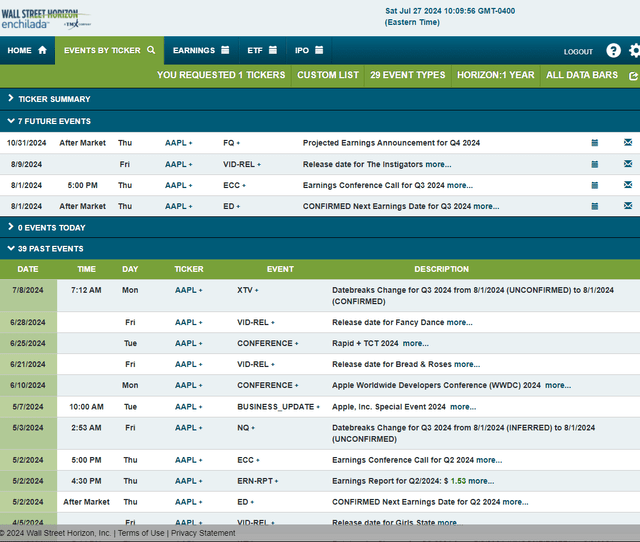

Wanting forward, company occasion knowledge offered by Wall Road Horizon present a confirmed Q3 2024 earnings date of Thursday, August 1 AMC with a convention name instantly after the numbers cross the wires. You possibly can pay attention reside right here. No different volatility catalysts are seen on the calendar.

Company Occasion Danger Calendar

Wall Road Horizon

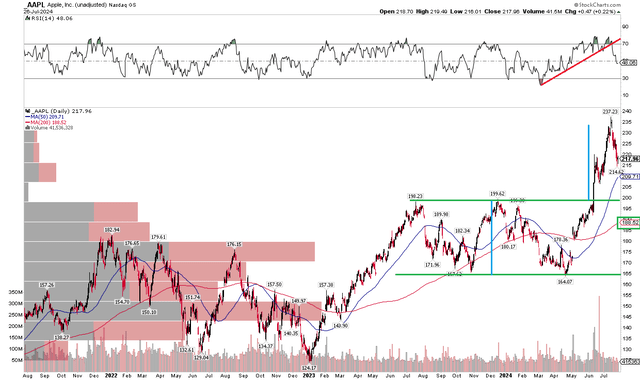

The Technical Take

With shares undervalued in my opinion and amid constructive headlines surrounding the inventory, AAPL’s technical scenario is constructive. Discover within the chart beneath that shares broke out from a monthslong consolidation vary from the mid-$160s on the low finish to only shy of $200 on the higher finish.

However shares stalled out close to $237 earlier this month, which was very near the measured transfer worth goal primarily based on the $35 earlier vary’s peak. I see long-term help at earlier resistance ranges, close to $200.

Additionally check out the RSI momentum oscillator on the prime of the graph. I have to acknowledge that momentum has certainly rolled over amid the broader tech selloff this month. I additionally don’t like that the Nasdaq Composite is struggling throughout what’s often a constructive interval on the calendar.

However, AAPL’s long-term 200-day transferring common is positively sloped, suggesting that the bulls management the first pattern. Furthermore, there’s a excessive quantity of quantity by worth if the inventory dips underneath $200, so shopping for on a post-earnings dip, if we get it, needs to be seen as a shopping for alternative.

General, $198 to $200 is help, whereas the $237 all-time excessive is resistance.

AAPL: Bullish Breakout, Key Help at $200, Rising 200dma

Stockcharts.com

The Backside Line

I’ve a purchase ranking on Apple. I see the megacap as a renewed development story whereas the corporate continues to reward shareholders via dividends and buybacks. With shares about 10% beneath my intrinsic worth goal, the chart scenario is mostly wholesome after the long-term upside breakout final quarter.

Scholar protests in opposition to Israel’s offensive in Gaza unfold – Cyber Tech

EU to hit Chinese language electrical automobiles with tariffs of as much as 48% – Cyber Tech

French PM Michel Barnier to type authorities ‘subsequent week’ – Cyber Tech

About The Author

admin

Azeem Rajpoot, the author behind This Blog, is a passionate tech enthusiast with a keen interest in exploring and sharing insights about the rapidly evolving world of technology. With a background in Blogging, Azeem Rajpoot brings a unique perspective to the blog, offering in-depth analyses, reviews, and thought-provoking articles. Committed to making technology accessible to all, Azeem strives to deliver content that not only keeps readers informed about the latest trends but also sparks curiosity and discussions. Follow Azeem on this exciting tech journey to stay updated and inspired.