Berkshire Dumping Apple Is Completely A Promote Sign (Score Downgrade) – Cyber Tech

JohanSjolander

It was introduced this weekend that Berkshire Hathaway Inc. (BRK.A) (BRK.B) continues to liquidate its huge Apple Inc. (NASDAQ:AAPL) holdings, possible as quick as it might with out torpedoing the share quote. The Q2 2024 report’s spotlight was the promoting of round 390 million shares in maybe the main Huge Tech identify on this planet, or about 50% of his place between March and June. Within the course of, Berkshire has spiked its money holdings to a document, at a tremendous quantity of $276 billion!

Is CEO Warren Buffett apprehensive about Apple’s China-focused provide chain as tensions with the U.S. soar? Probably. Is he involved about capital features tax charges rising subsequent 12 months, to assist slash the out-of-control U.S. fiscal deficit? He is mentioned as a lot, for my part. Is he trying ahead to slower client spending in a world recession, and its adverse impact on Apple’s working outcomes? Probably. Is he apprehensive {that a} $3 trillion firm can not compound cash at an above-average price due to its sheer measurement? Greater than possible.

But, the #1 cause to be promoting Apple now, for my part, might revolve round its clear overvaluation vs. previous buying and selling, and the construction of rates of interest within the bond market. I’ve been screaming about this for over a 12 months now in my earlier articles on the inventory. Proudly owning an overpriced, slow-growth blue chip with rates of interest within the 4% to five% vary makes little mathematical sense, even when it is the Apple model identify.

Exterior of founder Steve Jobs, Mr. Buffett has been maybe the most important Apple cheerleader over the corporate’s storied historical past. So, when his view sours, all Apple traders ought to take notice. Is Mr. Buffett’s determination to promote shares for round $200 a warning sign to small retail traders? Completely.

The Overvaluation Drawback

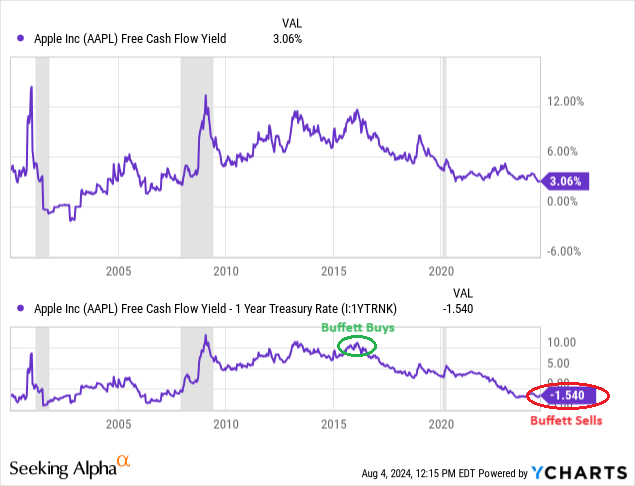

The first valuation drawback is barely rising free money circulate yields of three%, that are a whole failure vs. 5% cash-investment returns for my part. Buffett started buying his place in 2016, when free money circulate yields of 11%+ have been obtainable vs. “risk-free” money yields lower than 2% (utilizing prevailing 1-year Treasury charges), the other of as we speak’s setup. When it comes to shopping for a inventory with a low valuation and promoting it at a excessive one, Buffett’s commerce might go down in historical past as “the” traditional round-trip commerce for its unimaginable greenback measurement, particularly if Apple is sitting on the identical quote as 2024’s excessive in 5-10 years (which I consider is completely attainable mathematically talking).

YCharts – Apple, Free Money Movement Yield vs. 1-12 months Treasury Fee, Since 2000, Writer Reference Factors

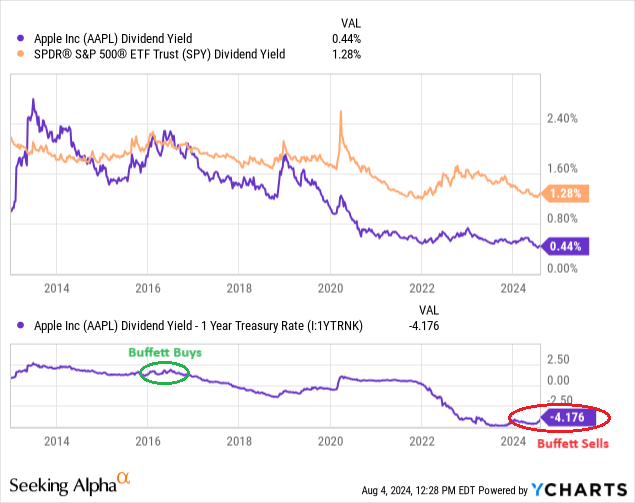

Additional, when Berkshire acquired Apple shares, the annual money dividend yield was 2.2%, about the identical because the S&P 500 index common and significantly higher than 1-year Treasury charges in 2016. The present dividend story of 0.44% vs. money investments returning nearer to five% is a rotten concept to purchase into, particularly contemplating the fairness worth threat inherent in your determination (100% of your funding might theoretically be misplaced) vs. the all-but-guaranteed 100% return of your capital.

YCharts – Apple, Dividend Yield vs. S&P 500 ETF & 1-12 months Treasury Fee, 10 Years

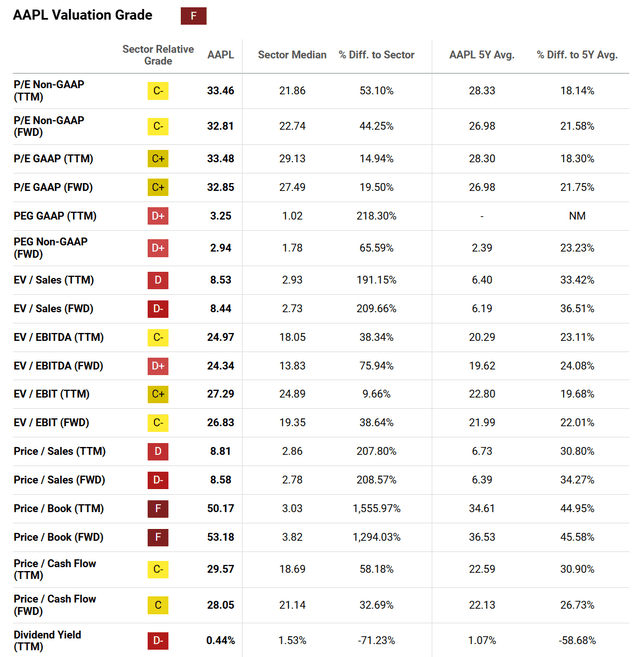

Anyway, Searching for Alpha’s computer-ranking system places an general “F” score on Apple for a Quant Valuation Grade. While you undergo all the basic metrics obtainable to assessment the share’s worth vs. underlying price, there’s not a lot there to again up your funding. SA Quant’s formulation seems to be at Apple’s 5-year buying and selling historical past, plus present monetary evaluation ratios vs. friends/opponents within the know-how business.

Searching for Alpha Desk – Apple, Quant Valuation Grade, August 2nd, 2024

Technical Buying and selling Reversal Underway

I used to be already fairly nervous about Apple’s funding future, earlier than Buffett introduced he was promoting months in the past. That is two strikes in opposition to this fairness. The third strike has appeared because the finish of July: quite a few technical reversal indicators have popped up as extra proof that one thing is amiss.

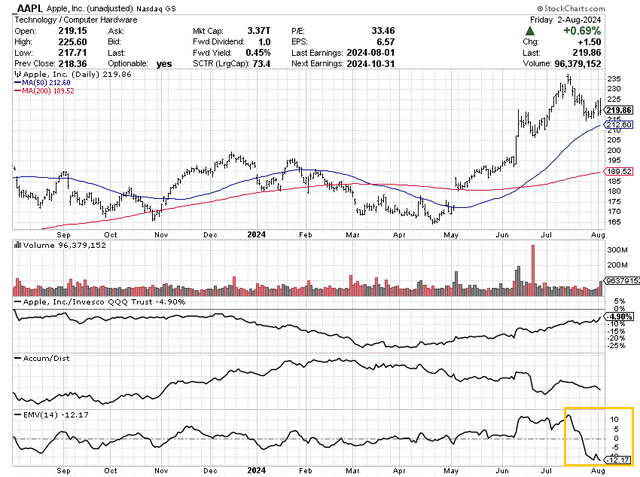

Certain, Apple has underperformed the NASDAQ 100 index for a while, as referenced within the comparability line vs. the Invesco QQQ Belief (QQQ) drawn under. After years of regular will increase within the Accumulation/Distribution Line, Berkshire’s promoting is clearly seen within the downtrending slope since February.

Maybe most enlightening (and really scary) as an instantaneous indicator concern for Apple shareholders is the brand new all-time low within the 14-day Ease of Motion calculation. In actual fact, transferring from a document excessive three weeks in the past to a document low over a comparatively brief time period is uncommon (boxed in gold). It’s often related to severe promoting volumes vs. an absence of shopping for curiosity. When it is “simple” to maneuver the value decrease, like in July, the EMV usually screams that now could be the time to promote.

Is my EMV sign foolproof and all the time appropriate for timing a promote? No. Typically worth bottoms proper after an EMV blowout decline and heads greater. Different circumstances, nevertheless, have confirmed its usefulness as a terrific timing machine, predicting that far weaker quotes are coming over the following weeks, months, and even years.

StockCharts.com – Apple, 12 Months of Each day Worth & Quantity Modifications, Writer Reference Level

Let’s undergo some historic Apple charts of how all-time lows within the 14-day EMV studying have fared in earlier bear markets and recessions. In all honesty, I believe Buffett might have been capable of get out at peak pricing during the last a number of months.

2021-22

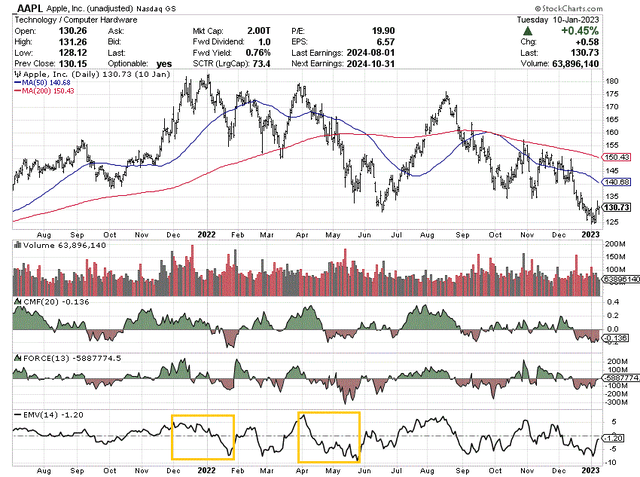

The final occasion of two swings from document highs to lows (at the moment) within the EMV got here close to Apple’s main high in late 2021, adopted by one other pivot to heavy promoting in Could 2022. Each are boxed in gold once more under. Apple’s quote would find yourself declining by almost -40% from its early January peak above $182 into January 2023.

StockCharts.com – Apple, Each day Worth & Quantity Modifications, July 2021 to Jan 2023, Writer Reference Factors

2020

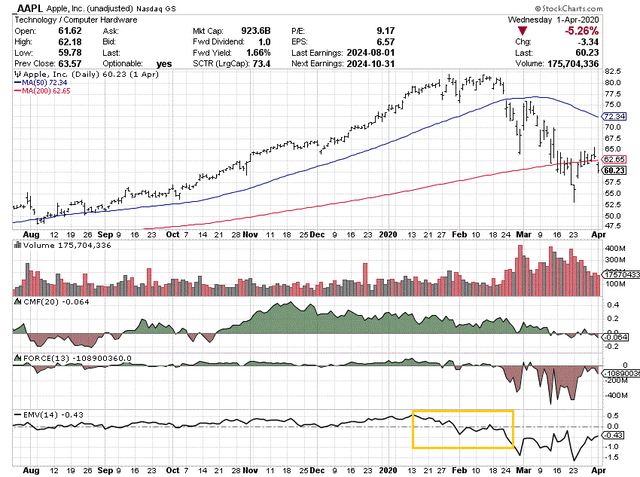

Though short-lived for a selloff, the following sign got here within the early days of the pandemic. Worth would implode one other -30% quickly from the purpose of all-time lows (roughly -40% peak to trough), however recovered rapidly.

StockCharts.com – Apple, Each day Worth & Quantity Modifications, July 2019 to March 2020, Writer Reference Level

2018

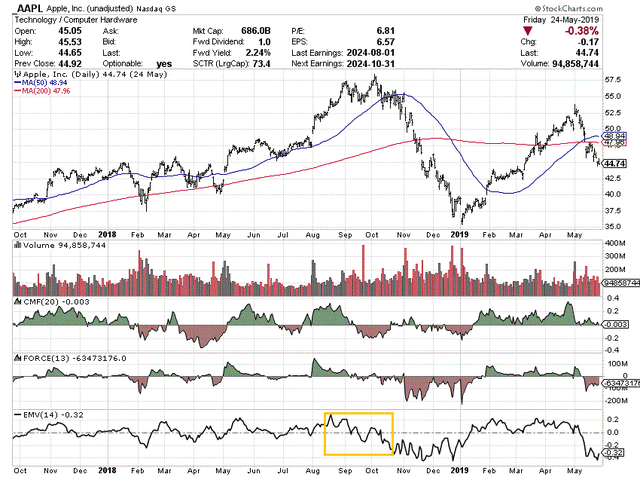

Earlier than that, 2018’s reversal proved to be one other EMV sign winner for timing your promote. The section change from greed to worry was fairly pronounced on this early warning indicator. And, you can have gotten out earlier than a -40% worth implosion over 10 weeks.

StockCharts.com – Apple, Each day Worth & Quantity Modifications, Sept 2017 to Could 2019, Writer Reference Level

2007-08

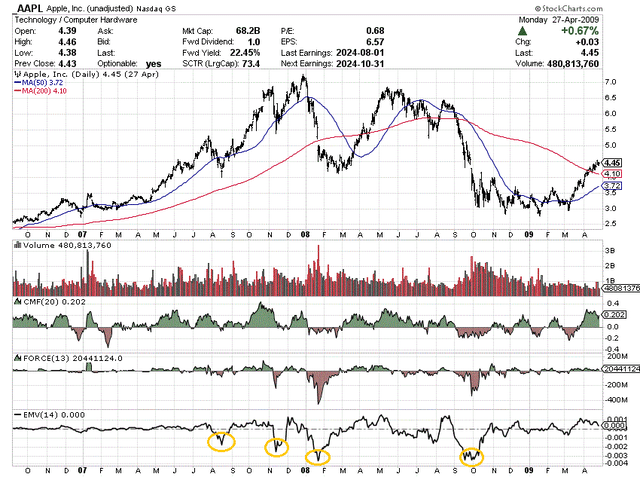

How did the EMV assemble do in the course of the 2007-09 Nice Recession interval? Properly, new all-time lows within the indicator are circled in gold under. The primary sign proved just a little early throughout August 2007 as Apple’s worth continued one other +35% greater. However a string of latest lows have been reached later that 12 months and early 2008. Worth would find yourself declining by -60% from its December 2007 peak, and -30% measured from the “first” sign into January 2009.

StockCharts.com – Apple, Each day Worth & Quantity Modifications, Sept 2006 to Apr 2009, Writer Reference Factors

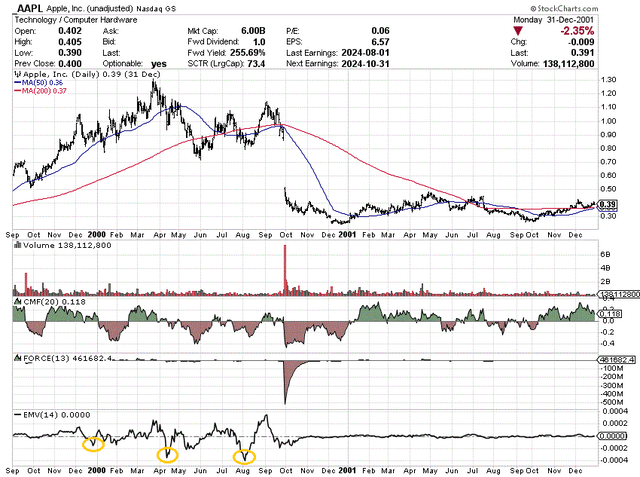

1999-2001

The unique Nineteen Nineties Dotcom bubble burst seemed much like the Nice Recession EMV and worth sample from Apple. The primary sign in December 1999 proved untimely, whereas the second got here proper after its precise worth peak, and the third warning appeared weeks earlier than the underside dropped out of its quote. From the March 2000 excessive, a complete decline of -85% ran its course by December 2020. Afterward, the value didn’t recuperate for years.

StockCharts.com – Apple, Each day Worth & Quantity Modifications, Sept 1999 to Dec 2001, Writer Reference Factors

Remaining Ideas

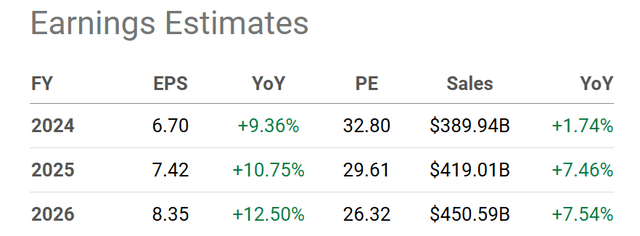

Working enterprise progress has already been subpar vs. the Huge Tech group since 2021. Analyst estimates are upbeat for 2024-26, however forecasted charges of enhance are nonetheless a far cry from previous progress charges or these projected from the NASDAQ 100 index as a complete.

Searching for Alpha Desk – Apple, Analyst Estimates for 2024-26, Made August 2nd, 2024

So, it appears to me that Buffett has determined to cash-in his chips at a excessive worth, which, I consider, is the one viable threat/reward choice. Heck, Berkshire can earn dramatically extra in curiosity on money, with an almost “risk-free” assured return of his upfront capital. My query is: Why are you holding or shopping for Apple at costs over $200 per share?

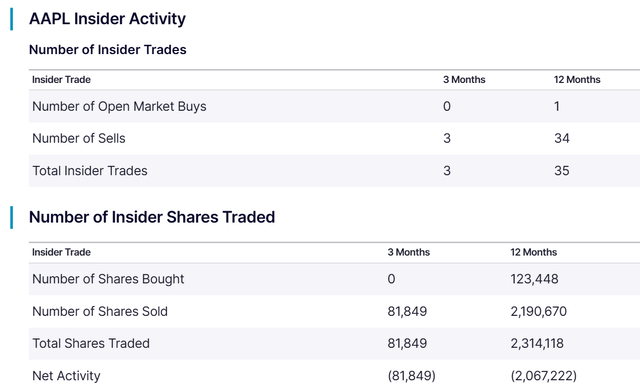

It seems to me that insiders and administration can’t discover sufficient good causes to buy Apple at its lofty valuation, both. In actual fact, there has solely been one buy vs. 34 promote trades during the last 12 months reported to the SEC. A internet of two,314,118 shares have been “formally” bought, exterior of Buffett’s rush to the exits.

Nasdaq.com – Apple, Insider Buying and selling Exercise, Previous 12 Months

My view is prudent and cheap traders needs to be ready for materially decrease costs to purchase, and long-time shareholders ought to severely ponder transferring on, simply as Berkshire is doing. I consider a -20% to -50% worth dump may very well be on the playing cards, with the worst returns skilled in a recession that sends gross sales and EPS decrease at Apple, not greater. Do not say it might’t occur. Outsized Apple share worth declines have routinely taken place over the a long time.

What might hold the value above $200 a share? Little question, this can be a nice query. The reply is a “Goldilocks” financial system, having fun with a steep slide in rates of interest and inflation, matched in opposition to rising client spending. This soft-landing situation continues to be the traditional knowledge expectation on Wall Avenue. I’m not saying such an occasion won’t happen.

It’s also attainable the EMV promote sign is untimely, similar to in late 1999 or the center of 2007. I might place the statistical odds of this being the case at 25% to 33%.

Nevertheless, if any new “black swan” promote catalyst exhibits up, a tough touchdown with doubtlessly a deep recession may very well be on faucet throughout 2025. For instance, what if crude oil costs double to US$150 a barrel quickly because of the Center East bother spilling over into navy battle within the crucial delivery lanes of the Persian Gulf? Then, inflation and rates of interest will virtually absolutely rise, whereas the struggling financial system is actually pushed into contraction. Beneath this situation, an Apple share quote of $100-$125 is completely possible. (A normalized P/E of 20x EPS declining to $6 would appear applicable, if rates of interest don’t come down in lockstep with a rotten financial system). It might be the dreaded double-whammy of falling valuation ratios on materially decrease gross sales and earnings.

With the unhealthy information piling up, I’ve determined to downgrade Apple to Sturdy Promote for a 12-month outlook. Even Warren Buffett, thought of one of many all-time finest funding minds, appears to agree that now could be the time to exit this safety.

Thanks for studying. Please take into account this text a primary step in your due diligence course of. Consulting with a registered and skilled funding advisor is really helpful earlier than making any commerce.

Obituary: Joanne J. Nelson – Door County Pulse – Cyber Tech

Navigating the AI craze | Inoreader weblog – Cyber Tech

Swiatek expande su hegemonía al conquistar por primera vez Madrid | Tenis | Deportes – Cyber Tech

About The Author

admin

Azeem Rajpoot, the author behind This Blog, is a passionate tech enthusiast with a keen interest in exploring and sharing insights about the rapidly evolving world of technology. With a background in Blogging, Azeem Rajpoot brings a unique perspective to the blog, offering in-depth analyses, reviews, and thought-provoking articles. Committed to making technology accessible to all, Azeem strives to deliver content that not only keeps readers informed about the latest trends but also sparks curiosity and discussions. Follow Azeem on this exciting tech journey to stay updated and inspired.